")

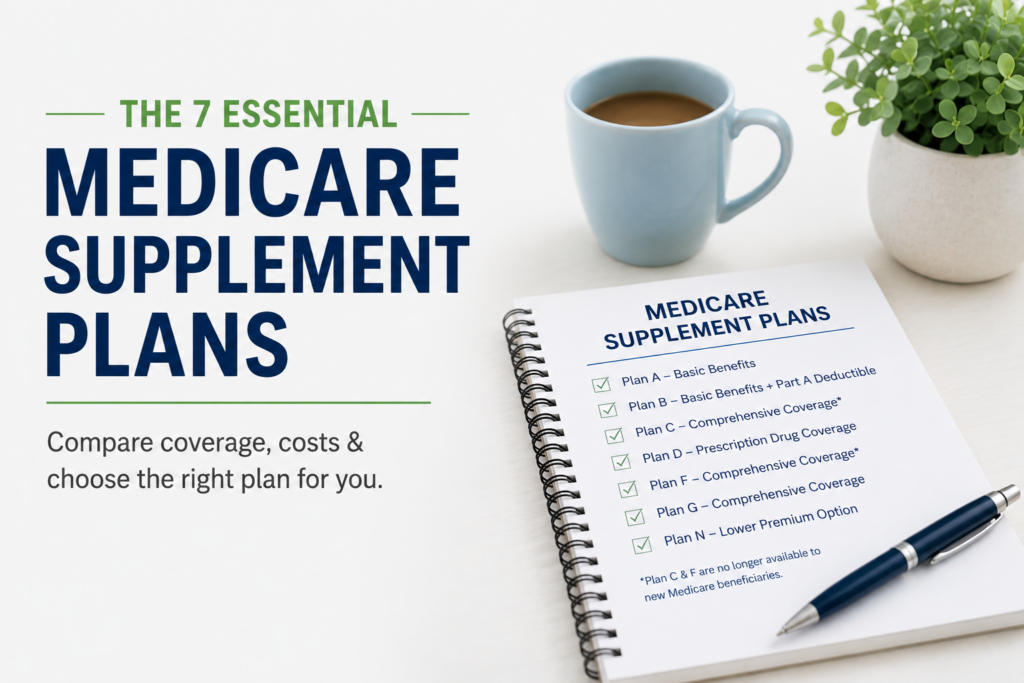

7 Essential Medicare Supplement Plans

Find An Agent

Search your ZIP code to find trusted Medicare agents near you.

Trusted by Thousands of Seniors Nationwide

7 Essential Medicare Supplement Plans

Medicare offers 10 standardized Supplement plans labeled A through N, but most seniors turning 65 compare just a handful. Plan G is the most popular choice, covering nearly all out-of-pocket costs except the Part B deductible. Plan N offers lower premiums with small copayments. The right plan depends on your health, budget, and how often you use medical care.

Former president Harry Truman received the first Medicare card on July 30, 1965, the day it was signed into law by then-president Lyndon Johnson. Medicare coverage took effect in 1966 with a budget of approximately $10 billion and about 19 million enrollees.

Medicare Supplement plans were created in the 1980s under a piece of legislation called the Baucus Amendment to provide Medicare recipients with coverage for gaps in Medicare. Today, about 87% of traditional Medicare beneficiaries have additional coverage that supplements Medicare benefits. Two in ten Medicare beneficiaries have Medicare supplement insurance, and roughly 43% of Original Medicare beneficiaries have supplemental coverage through employer plans, Medicaid, or Medigap, with about 20% specifically enrolled in Medigap.

What Exactly Is Medigap?

Original Medicare, Parts A and B, covers a wide range of healthcare services, including hospital stays, doctor visits, laboratory work and preventive care. Medigap plans act as a secondary payer, covering out-of-pocket costs like copayments, coinsurance and deductibles once Medicare approves the service.

Medigap plans are offered by private health insurance companies. Regulated by both state governments and the federal one, these Medicare Supplement plans pay a portion of the bill not paid by Medicare.

Because Medigap plans don’t include prescription drug coverage, enrollees need a separate Medicare Part D plan to cover medications. Such plans can’t deny claims that Medicare has already approved. Medigap itself does not use provider networks or referrals, though Medicare coverage rules may still apply.

The Medigap Open Enrollment Period generally begins on the first day of the month in which you are both age 65 or older and enrolled in Medicare Part B, and lasts for six months. The premiums for this type of plan differ based on the plan and company from which it is purchased.

There are ten standardized Medicare supplement plans, identified by the letters A, B, C, D, F, G, K, L, M, and N, and Medigap plans are standardized across most of the United States. Although the core benefits for each plan letter are the same, availability, pricing, underwriting rules and added perks, such as dental and vision, vary by state and ZIP code. The primary difference between insurers is the cost of the premium.

Comparing the 7 Most Essential Medigap Plans

Selecting a Medigap policy that best fits your health concerns and financial circumstances enables you to realize more predictable healthcare costs and avoid costly surprise medical bills. Plus, Medigap works with any provider that accepts Medicare, so you’re covered without having to select from a small pool of providers.

Plan G

Plan G is considered the most comprehensive Medigap plan available to new enrollees. It’s a top choice for Medicare beneficiaries with broad coverage needs because it covers everything except the annual Part B deductible, projected at $283 in 2026. As the most popular Medigap choice for new buyers seeking nearly all-inclusive protection, Plan G offers high-value coverage for doctor visits, hospital stays and foreign travel emergencies.

| Benefit | Coverage Details | Covered? |

| Part A Hospital Coinsurance | 100% of Part A coinsurance for hospital stays, plus an additional 365 days after Medicare benefits run out | ✔ Covered |

| Part A Hospital Deductible | Covers the full Part A deductible ($1,736 in 2026) | ✔ Covered |

| Part B Coinsurance/Copayment | Covers the remaining 20% after Medicare pays 80% of approved services | ✔ Covered |

| Part B Excess Charges | Covers up to 15% above the Medicare-approved amount if a doctor does not accept Medicare assignment | ✔ Covered |

| Skilled Nursing Facility Coinsurance | Covers the daily coinsurance for days 21–100 in a skilled nursing facility | ✔ Covered |

| Part A Hospice Care Coinsurance/Copayment | Covers your share of hospice care costs under Part A | ✔ Covered |

| Foreign Travel Emergency | Covers 80% of approved emergency medical costs outside the U.S., up to plan limits | ✔ Covered |

| Part B Deductible | You pay the annual Part B deductible (projected at $283 in 2026) | X Not Covered |

| Prescription Drugs | A separate Medicare Part D prescription drug plan is needed | X Not Covered |

Elements to look for in a Plan G carrier include strong financial stability, low customer complaint rates, competitive premiums, household discounts in many states, personalized local agent support, strong customer service reputations and wide availability across most states.

Plan N

Plan N offers lower premiums than Plan G in exchange for modest copays and limitations on excess charge coverage. It is among the fastest-growing Medigap plan types, covering 10% of policyholders. Plan N covers the same key gaps as Plan G, but enrollees are responsible for Part B excess charges and copays of up to $20 for office visits and $50 for emergency department visits that don’t result in hospitalization.

| Benefit | Coverage Details | Covered? |

| Part A Hospital Coinsurance | 100% of Part A coinsurance for hospital stays, plus an additional 365 days after Medicare benefits run out | ✔ Covered |

| Part A Hospital Deductible | Covers the full Part A deductible ($1,736 in 2026) | ✔ Covered |

| Part B Coinsurance/Copayment | Covers Part B coinsurance, except a copay of up to $20 for office visits and up to $50 for ER visits that do not result in hospitalization | ✔ Covered with copays |

| Skilled Nursing Facility Coinsurance | Covers the daily coinsurance for days 21–100 in a skilled nursing facility | ✔ Covered |

| Part A Hospice Care Coinsurance/Copayment | Covers your share of hospice care costs under Part A | ✔ Covered |

| Foreign Travel Emergency | Covers 80% of approved emergency medical costs outside the U.S., up to plan limits | ✔ Covered |

| Part B Excess Charges | You are responsible for any excess charges if a doctor does not accept Medicare assignment | X Not Covered |

| Part B Deductible | You pay the annual Part B deductible (projected at $283 in 2026) | X Not Covered |

| Prescription Drugs | A separate Medicare Part D prescription drug plan is needed | X Not Covered |

The ideal audience for Plan N is enrollees comfortable with some per-visit costs in return for much lower premiums. Plan N premiums range from $85 to $200, with national averages from $120 to $180.

Plan F

As the only Medigap plan that covers all nine standardized benefits and pays for all Original Medicare out-of-pocket costs, Plan F offers the most complete coverage. It’s not available to enrollees who became Medicare-eligible after January 1, 2020, but it remains an important choice for those grandfathered in.

| Benefit | Coverage Details | Covered? |

| Part A Hospital Coinsurance | 100% of Part A coinsurance for hospital stays, plus an additional 365 days after Medicare benefits run out | ✔ Covered |

| Part A Hospital Deductible | Covers the full Part A deductible ($1,736 in 2026) | ✔ Covered |

| Part B Coinsurance/Copayment | Covers the remaining 20% after Medicare pays 80% of approved services | ✔ Covered |

| Part B Deductible | Covers the full annual Part B deductible (projected at $283 in 2026) | ✔ Covered |

| Part B Excess Charges | Covers up to 15% above the Medicare-approved amount if a doctor does not accept Medicare assignment | ✔ Covered |

| Skilled Nursing Facility Coinsurance | Covers the daily coinsurance for days 21–100 in a skilled nursing facility | ✔ Covered |

| Part A Hospice Care Coinsurance/Copayment | Covers your share of hospice care costs under Part A | ✔ Covered |

| Foreign Travel Emergency | Covers 80% of approved emergency medical costs outside the U.S., up to plan limits | ✔ Covered |

| Prescription Drugs | A separate Medicare Part D prescription drug plan is needed | X Not Covered |

Plan F premiums are based on age, gender and geographic area. Standard premiums range from $241 to $400 monthly, while high-deductible plans average $62 to $100 per month after the $2,950 deductible is reached.

Average 2026 Plan F premiums:

- Age 65–69: $150–$300/month

- Age 70–74: $175–$350/month

- Age 75–79: $200–$425/month

- Age 80+: $250–$500+/month

Plan A

Plan A is the most basic standardized Medigap plan. In some states, it may be the only Medigap option available to beneficiaries under 65 who qualify due to disability. It covers essential hospital and medical coinsurance but omits skilled nursing, Part B excess charges and foreign travel emergency care. It’s often the best option for enrollees who want low premiums and minimal supplemental coverage.

| Benefit | Coverage Details | Covered? |

| Part A Hospital Coinsurance | 100% of Part A coinsurance for hospital stays, plus an additional 365 days after Medicare benefits run out | ✔ Covered |

| Part B Coinsurance/Copayment | Covers the remaining 20% after Medicare pays 80% of approved services | ✔ Covered |

| Part A Hospice Care Coinsurance/Copayment | Covers your share of hospice care costs under Part A | ✔ Covered |

| Part A Hospital Deductible | You pay the full Part A deductible ($1,736 in 2026) | X Not Covered |

| Skilled Nursing Facility Coinsurance | You pay the daily coinsurance for days 21–100 in a skilled nursing facility | X Not Covered |

| Part B Deductible | You pay the annual Part B deductible (projected at $283 in 2026) | X Not Covered |

| Part B Excess Charges | You are responsible for any excess charges if a doctor does not accept Medicare assignment | X Not Covered |

| Foreign Travel Emergency | Emergency medical costs outside the U.S. are not covered | X Not Covered |

| Prescription Drugs | A separate Medicare Part D prescription drug plan is needed | X Not Covered |

Plan K

Plan K is designed to assist with out-of-pocket costs such as coinsurance, copayments and deductibles not fully covered by Original Medicare. Its cost-sharing approach results in lower premiums, but enrollees pay higher out-of-pocket costs. However, Plan K includes an out-of-pocket limit of $8,000 in 2026, after which 100% of cost-sharing expenses are covered for the rest of the calendar year.

| Benefit | Coverage Details | Covered? |

| Part A Hospital Coinsurance | 100% of Part A coinsurance for hospital stays, plus an additional 365 days after Medicare benefits run out | ✔ Covered (100%) |

| Part A Hospital Deductible | Covers 50% of the Part A deductible ($1,736 in 2026) | ✔ Covered (50%) |

| Part B Coinsurance/Copayment | Covers 50% of the Part B coinsurance or copayment after Medicare pays its share | ✔ Covered (50%) |

| Part A Hospice Care Coinsurance/Copayment | Covers 50% of your share of hospice care costs under Part A | ✔ Covered (50%) |

| Skilled Nursing Facility Coinsurance | Covers 50% of the daily coinsurance for days 21–100 in a skilled nursing facility | ✔ Covered (50%) |

| Annual Out-of-Pocket Limit | Once you reach the $8,000 out-of-pocket limit in 2026, Plan K pays 100% of covered Medicare costs for the rest of the calendar year | ✔ Covered |

| Part B Deductible | You pay the full annual Part B deductible (projected at $283 in 2026) | X Not Covered |

| Part B Excess Charges | You are responsible for any excess charges if a doctor does not accept Medicare assignment | X Not Covered |

| Foreign Travel Emergency | Emergency medical costs outside the U.S. are not covered | X Not Covered |

| Prescription Drugs | A separate Medicare Part D prescription drug plan is needed | X Not Covered |

Plan L

Plan L is designed for enrollees who want more coverage than Plan K but don’t want to pay the higher premiums of Plans G or N. It’s a good option for Medicare beneficiaries who are generally healthy, rarely use specialists, and want a meaningful safety net without a large monthly bill. Plan L offers a middle path compared to other Medigap plans, with modest cost-sharing on routine care and a $4,000 out-of-pocket cap.

| Benefit | Coverage Details | Covered? |

| Part A Hospital Coinsurance | 100% of Part A coinsurance for hospital stays, plus an additional 365 days after Medicare benefits run out | ✔ Covered (100%) |

| Part A Hospital Deductible | Covers 75% of the Part A deductible ($1,736 in 2026) | ✔ Covered (75%) |

| Part B Coinsurance/Copayment | Covers 75% of the Part B coinsurance or copayment after Medicare pays its share | ✔ Covered (75%) |

| Part A Hospice Care Coinsurance/Copayment | Covers 75% of your share of hospice care costs under Part A | ✔ Covered (75%) |

| Skilled Nursing Facility Coinsurance | Covers 75% of the daily coinsurance for days 21–100 in a skilled nursing facility | ✔ Covered (75%) |

| Annual Out-of-Pocket Limit | Once you reach the $4,000 out-of-pocket limit in 2026, Plan L pays 100% of covered Medicare costs for the rest of the year | ✔ Covered |

| Part B Deductible | You pay the full annual Part B deductible (projected at $283 in 2026) | X Not Covered |

| Part B Excess Charges | You are responsible for any excess charges if a doctor does not accept Medicare assignment | X Not Covered |

| Foreign Travel Emergency | Emergency medical costs outside the U.S. are not covered | X Not Covered |

| Prescription Drugs | A separate Medicare Part D prescription drug plan is needed | X Not Covered |

High-Deductible Plan G

High-Deductible Plan G is essentially the standard Plan G, but enrollees pay all Medicare-approved out-of-pocket costs until reaching a $2,950 deductible in 2026. After that deductible is met, the plan covers costs the same as standard Plan G. Monthly premiums for High-Deductible Plan G range from $40 to $80 compared to $150 to $220 for standard Plan G.

| Benefit | Coverage Details | Covered? |

| Annual Deductible | You pay all Medicare-approved out-of-pocket costs up to $2,950 in 2026 before the plan begins paying | Pay First |

| Part A Hospital Coinsurance | After the deductible is met, covers 100% of Part A coinsurance for hospital stays, plus an additional 365 days after Medicare benefits run out | ✔ After Deductible |

| Part A Hospital Deductible | After the deductible is met, covers the full Part A deductible ($1,736 in 2026) | ✔ After Deductible |

| Part B Coinsurance/Copayment | After the deductible is met, covers the remaining 20% after Medicare pays 80% of approved services | ✔ After Deductible |

| Part B Excess Charges | After the deductible is met, covers up to 15% above the Medicare-approved amount if a doctor does not accept Medicare assignment | ✔ After Deductible |

| Skilled Nursing Facility Coinsurance | After the deductible is met, covers the daily coinsurance for days 21–100 in a skilled nursing facility | ✔ After Deductible |

| Part A Hospice Care Coinsurance/Copayment | After the deductible is met, covers your share of hospice care costs under Part A | ✔ After Deductible |

| Foreign Travel Emergency | After the deductible is met, covers 80% of approved emergency medical costs outside the U.S., up to plan limits | ✔ After Deductible |

| Part B Deductible | The Part B deductible, projected at $283 in 2026, counts toward your $2,950 plan deductible but is not separately covered | X Not Covered |

| Prescription Drugs | A separate Medicare Part D prescription drug plan is needed | X Not Covered |

Tips for Choosing the Right Medigap Plan

Medicare covers a lot but not everything. Costs from deductibles, coinsurance, copayments, and excess charges can add up quickly. This step-by-step guide was created to help you select the right plan letter for your health and budget.

Step #1: Match Plan Letters to Your Risk Tolerance

| If you… | Plan |

| Want zero surprises, see doctors often | G |

| Want near-G coverage at lower premiums, few specialist visits | N |

| Were Medicare-eligible before 2020, want everything covered | F |

| Are healthy with savings, want low premiums | High-Deductible G |

| Want moderate cost-sharing with a $4,000 OOP cap | L |

| Want maximum savings with an $8,000 OOP cap | K |

| Need basic coverage only | A |

Step #2: Factor In Your Health and Physicians

- Chronic conditions or frequent specialist visits: Plans G or N pay off long-term.

- Expecting surgery or heavy usage: Avoid High-Deductible G; you’ll likely hit the deductible every year.

- Doctors who don’t accept Medicare assignment: Only Plans F and G cover excess charges.

- International travel: Plans A, B, K and L do not cover foreign emergencies.

Step #3: Collect Geographic-Specific Quotes

Premiums for the same letter can vary in the same geographic location. Get at least three quotes, and search for Medicare agents by location.

Step #4: Compare Insurers

| Factor | What to Look For |

| Pricing method | Community-rated stays stable; attained-age rises with age |

| Rate increase history | Avoid insurers with steep recent hikes |

| Financial strength | A.M. Best rating of A or higher |

| Complaint ratio | Lower NAIC index is better |

| Household discounts | 7%–12% off if a spouse or housemate also enrolls |

| Added perks | Vision, hearing or fitness discounts |

| Local agents | State Farm stands out for face-to-face service |

Step #5: Enroll at the Right Time

Your six-month Medigap Open Enrollment Period begins when you turn 65 and enroll in Part B. Insurance carriers cannot deny coverage or charge more for health conditions during this window. It’s one-time and never repeats, and missing it means medical underwriting applies.

Quick Decision Flowchart

Your Pre-Enrollment Checklist

- Chosen plan aligns with your healthcare needs and financial comfort level

- Verify that your preferred doctors accept Medicare assignment, or that your plan covers excess charges

- Confirm foreign travel emergency coverage if applicable

- Compare quotes from at least three insurers in your ZIP code

- Evaluate insurers based on pricing, rate increase history, and financial strength

- Check eligibility for household discounts or multi-policy discounts

- Enroll during your Medigap Open Enrollment Period or a guaranteed issue window

- Select a separate Medicare Part D prescription drug plan if needed

Comparing Medigap Coverage and Costs

Choosing a Medigap plan requires selecting the plan letter that best fits your health needs and budget and knowing which insurance carrier offers the best price and service for that letter. Benefits for each plan letter are set by federal law and are identical across all insurers, making it important to compare premiums, pricing methods, and any additional benefits such as dental and vision coverage.

Plan Comparison: Coverage at a Glance

100% = fully covered | — = not covered | † Plan N pays 100% of Part B coinsurance except up to $20 copay for some office visits and up to $50 for ER visits not resulting in admission.

| Plan | A Hosp. | B Coins. | A Ded. | SNF | Blood/Hosp. | B Ded. | Excess | Travel | Premium |

| Plan A | 100% | 100% | — | — | 100% | — | — | — | ~$80–$150 |

| Plan F* | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 80% | ~$150–$300 |

| Plan G | 100% | 100% | 100% | 100% | 100% | — | 100% | 80% | ~$100–$200 |

| HD Plan G | 100% | 100% | 100% | 100% | 100% | — | 100% | 80% | ~$40–$80 |

| Plan K | 100% | 50% | 50% | 50% | 50% | — | — | — | ~$50–$100 |

| Plan L | 100% | 75% | 75% | 75% | 75% | — | — | — | ~$70–$130 |

| Plan N | 100% | 100%† | 100% | 100% | 100% | — | — | 80% | ~$80–$160 |

*Plan F is available only to those eligible for Medicare before January 1, 2020.

Enrollment and Eligibility

Your enrollment window determines whether a Medigap insurer can ask you health questions, charge you more or deny coverage altogether. That’s why it’s especially important to know when to enroll.

| Window | When | What It Means |

| Open Enrollment Period | Six months starting when you turn 65 and enroll in Part B | Guaranteed issue, no health questions or denials, and best rates. One-time only. |

| Guaranteed Issue Rights | Losing employer coverage, leaving Medicare Advantage within 12 months, insurer bankruptcy, or moving out of a plan’s service area | Insurance carriers must sell you a policy without underwriting. Rights depend on the triggering event. |

| Birthday Rule | 60-day window after your birthday each year | Switch to the same plan letter with a new carrier without any health questions. Cannot change plan letters. |

| Outside All Windows | Any other time | Medical underwriting applies. Insurers may deny coverage, charge more or exclude pre-existing conditions for up to six months. |

Key Eligibility Rules

- Plans C and F are unavailable to anyone who became Medicare-eligible on or after January 1, 2020.

- Under-65 enrollees due to disability, ESRD or ALS: not all states require insurers to offer Medigap before age 65. Where available, premiums are typically two to four times higher. A full Open Enrollment Period applies again at age 65.

- Pre-existing conditions cannot be excluded during your Open Enrollment Period or a guaranteed issue window. Outside those periods, insurers may impose up to a six-month waiting period.

- Massachusetts, Minnesota and Wisconsin use their own Medigap frameworks, so standard plan letters do not apply in those states.

- Medigap covers one person per policy. Spouses must purchase separate policies.

- You cannot simultaneously enroll in Medigap and Medicare Advantage.

Frequently Asked Questions

What do Medicare Supplement plans cover?

Medigap plans cover out-of-pocket costs that Original Medicare doesn’t, such as deductibles, coinsurance, copayments and, depending on the plan, excess charges and foreign travel emergencies. Benefits are standardized by plan letter in most states, but Massachusetts, Minnesota, and Wisconsin use different Medigap frameworks.

Do Medicare Supplement plans include prescription drug coverage?

No. All Medigap plans require a separate Medicare Part D plan for drug coverage.

When can I enroll in a Medicare Supplement plan?

The best time to enroll in Medigap is during your six-month Open Enrollment Period, starting when you turn 65 and enroll in Part B. During this window, carriers cannot deny you, charge more or ask health questions. Outside of it, medical underwriting typically applies. Certain qualifying events can trigger guaranteed issue rights, allowing you to enroll in Medigap at other times.

Can I switch Medicare Supplement plans after enrolling?

Yes, but there are limitations. Some states have a Birthday Rule that gives you a window after your birthday each year to switch to the same plan letter with a different carrier without having to answer health questions. Outside that window, underwriting typically applies, meaning that switching to a more comprehensive plan letter is harder than shifting to equal or lesser coverage.

Who benefits most from Medicare Supplement insurance?

Medigap most benefits Medicare enrollees who see doctors frequently, have chronic conditions and want predictable costs without surprise bills. It’s also a good option for beneficiaries who want coverage anywhere Medicare is accepted or live in states where providers can charge above Medicare-approved rates.